6 March 2018

Before you go any further, know this:

- I own some stock (disclosure).

- Markets are copy and therefore the information in this post should be absorbed and the stock should be tracked.

- In my opinion, the stock becomes attractive when it drops to 10-12 levels.

- All the information in this post is based on a phone call to the Gujarat Poly Electronics office.

REASONS WHY IT MAKES SENSE TO CONSIDER/ADD GUJARAT POLY ELECTRONICS TO YOUR PORTFOLIO

- The company belongs to the reputed Polychem group of companies. The promoter pedigree is good.

- It was formed as a JV between AVX Electronics, USA – Polychem and Gujarat Industrial Investment Corporation Limited (GIIC) ro manufacture single layer and multi layer capacitors.

- Over time, the company was hit by competition by China and suffered losses.

- The business was restructured and AVX Electronics exited the business in 2016-17. Their share was bought by Polychem.

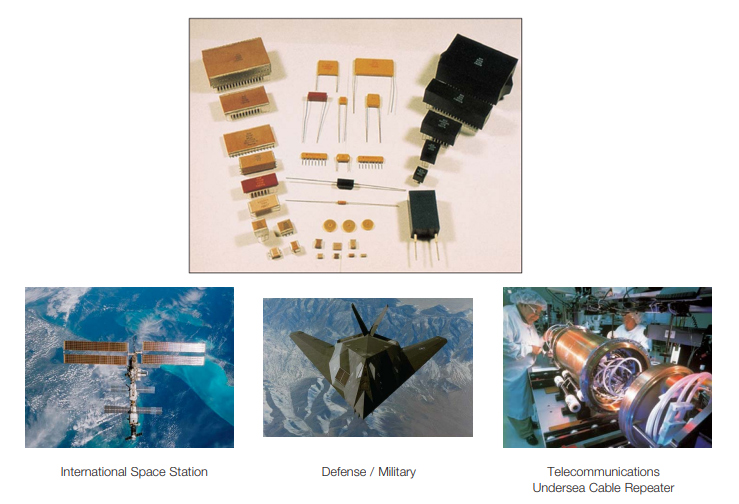

- In 2016-17, the company changed its strategy. It moved away from making the ordinary capacitors to value added capacitors (Radial Multi Layer Ceramic Capacitors) which are used in advanced applications like aerospace, telecommunications, defence, etc.

- One of the key ingredient of the new strategy was that the company would not produce capacitor parts. INSTEAD, it would import parts from China and assemble these to create Radial MLCCs.

- The company has since turned around and has started making modest profits. Turnover has increased in 2017-18 and the company should clock an EPS of about 75 paise for the year.

- The installed capacity for manufacturing MLCCs is 20 crore MLCCs per annum. However, there is no limit to MLCCs that are assembled.

- Radial MLCCs are priced between 35 paise and Rs 5 per piece, depending n their capacity. For the sake of approximation, let’s peg the average rate realized by Gujarat Poly Electronics at Rs 2.50 per MLCC.

- Let us assume that 2 years down the line, the company assembles and sells 14 crore MLCCs (70% of capacity). Its turnover will shoot to 40 crores. 2017-18 turnover will close at about 15 crores.

- The story does not stop here. The company has tied up with a MNC (Diotec Semicondustors, Germany) to distribute their products in India. The demand for semiconductors is rising phenomenally. The business potential of this new venture is not factored into the price.

These inputs are based on my conversation with Mr Punyani who is based at the company’s HO in Ahmedabad. I picked up the stock after this conversation and tweeted about it. This blog post is FYI.

Sir after recent price rise of up to 26 your view on Gujarat poly is still bullish ?

Check the next quarter’s results before making any decision

Similar question , can we still enter this stock at 38-39 for a long term ?

Can we still enter this stock at 38 – 39 rs for profit in a long term ? Or have we missed the bull rally and its time to focus on others ?

Thanks.

I think it’s better to focus elsewhere and watch how the next quarter plays out for this counter

After changing the business model there is turnaround case.

There is a demand and supply gap in Ceramic capacitors, Still there is a lot to go ahead sir….?

Keep watching results

Sir why they are not paying any tax?

Its a turnaround case. Old losses

Bad results sir

Sir any update on future prospects of guj poly

Nope. I got out i the 40s. It was recommended at 11. 300% n one year is good, no?

Sir,Can we consider for long term?