Here are the reasons why I consider Barak Valley Cements to have long term potential (read the negatives in red below):

- The company is based in the North East which should see phenomenal infrastructure development going forward. The Bharatmala,Interest subvention on affordable housing-food processing incentives, smart cities, development of new rail stations, etc., should see hectic demand for cement going forward.

- Management is clean.

- The company owns 5 operational subsidiary companies that are engaged in power generation, mining, tea cultivation and cement production business.Over time, it is possible that the company splits into several business divisions and makes investors rich.

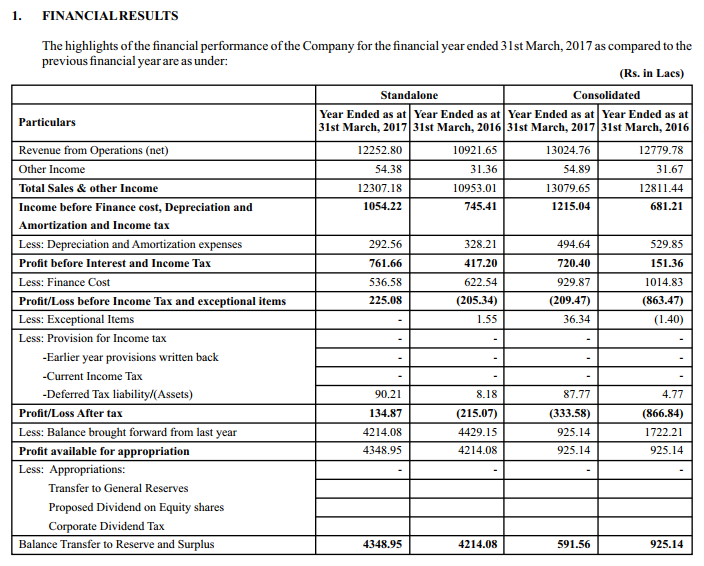

- Though the company made a profit on standalone basis in 2016-17, it ended up in a loss on consolidated basis. But it did make a cash profit – check the financials below.

- The company owns a cement brand (Valley Strong cement) whose equity is fast appreciating.

- During the last year, the company has increased its cement production capacity from 750 TPD Cement to 1000 TPD because of high demand.

- The Government of India’s Look East policy should witness infrastructure investments pouring into the North East regions and Barak valley is one of the leading cement producers out there.

- One of the major raw materials, limestone, is sourced from the company’s subsidiary. This gives the company an added edge.

- There are issues facing the company – low margins and losses from the power business. The first issue will be fixed as demand is set to increase. Power losses are reducing and over time, as electrification catches speed, will convert into profits.

- Another bugbear for the company is it’s debt – 56 crores (long term and short term). However, the company has expanded this year and the rising cement demand, or a new equity investor, should help them repay the new loan in quick time.The company has invested in and loaned about 52 crores to its power subsidiary where production has stalled because of non availability of raw material. In addition, the company has provided guarantees worth about 31 crores for it. This article is based on the assumption that raw material supplies will get better over time and that the power unit will be able to repay all its obligations.

- Promoter holds 57% of equity capital, and that is a good sign.

- The net cash flow from operations was +22 crores, and the investment in capacity addition worked out to 31 crores.

- The cash/cheques in hand at the end of the year were about 7 crores against crores last year, a healthy sign.

Barak Valley Cements is a slow burner. It is not a “phataka” stock that will go flying off. People with patience should keep tabs on its power project and future orders and perhaps consider investing in it with a time horizon of 3 years.

Discl: No interest