The stock I’m talking about is YASH PAPERS, a potential multibagger.

Without wasting your time in blah-blah, here are the reasons why:

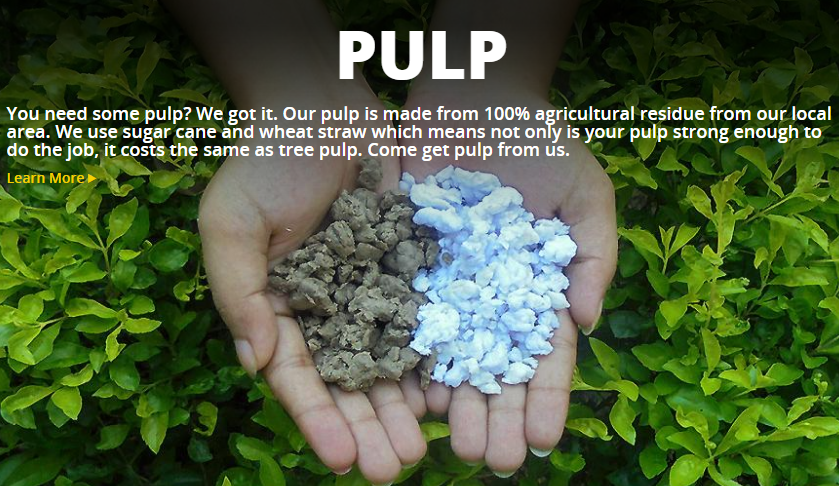

The company has 3 business divisions – Pulp, paper and moulded products (tableware).

Every division makes products that are made from agro waste (bagasse and rice husk).

The PULP division supplies unbleached bleached pulp to paper mills. Yash Papers makes pulp from agricultural waste – NO TREES ARE HACKED – making it an environment-friendly company.

Their MOULDED PRODUCT division has launched a new brand – CHUK! – which aims to replace styrofoam and plastic tableware with compostable and non-carcinogenic tableware made from agri waste (sugarcane bagasse). Presently, the company has launched tableware and egg trays.

At this point it is important to mention that France has already banned plastic tableware. Other developed nations may soon follow suit because plastics is ruining the environment and our oceans.

Many Indian states also have started banning the use of plastic disposables.

If you recall, the recent flooding in Mumbai, Chennai and Bangalore was largely caused because plastic stuff dumped in waste water channels choked up its outlets. Governments have two choices – penalize people for littering or reduce plastic use. As every political party needs votes, the chances of penalizing citizens is remote.

The third division, PAPER, manufactures packing and poster paper. This division will be benefitted by the retail, ecommerce and education boom that is upon us.

The opportunity for Yash Papers, in both the domestic and international market is humongous!

The company is a B CORP. A B Corp is a company that is set up to make profits AND is certified by a non-profit to the effect that the company meets exacting standards of social and environmental performance, accountability, and transparency.

In 2016-17, the company set up waste water recycling facilities and as per the annual report, consumes 190mn litres fewer daily.

The company also, in the previous year, has successfully emerged from its Corporate Debt Restructuring Mechanism. This has improved its creditworthiness and has lead to a reduction in interest. Taken with the general decrease in interest rates, the full benefits will be reflected in 2017-18.

On 21 September 2017, just next week, the company is launching its CHUK! range of environment-friendly tableware.

In the current year, apart from CHUK!, the company:

(a) is likely to increase its pulp and paper manufacturing capacity from 38,550 TPA to about 45,000 TPA with a marginal investment.

(b) will invest in automation (robots/newer machines) which will improve productivity and quality.

(c) will alter product mix and increase value-added products (coloured segment paper used in packing).

Yash Papers has 11.5-TPD capacity plant for manufacturing compostable tableware by investing 58 crore using debt and equity. The company plans to scale up the capacity to 23-TPD in 2018-19. The company has appointed distributors in India and is working to create awareness of its products in the mature markets of US, Europe and Australia.

100% of Yash Paper’s energy needs are met by renewable energy from its own captive biomass-based power plant that consumes rice husk as fuel.

Though India is being digitized, the growth in ecommerce, retail, packaging, document storage and education will keep the demand for paper in a robust mood.

Recently, the FSSAI has banned the packing of food in newspapers because it can cause lead poisoning. This is extremely bullish news for Yash Papers.

The company has appointed Mrs. Kimberly Ann McArthur as an International Marketing Consultant to tap into the developed markets.

The company’s EBITDA margin is 17%, ROCE is 19.4%, Debt-Equity is a healthy 1.32, and EPS was Rs 2 for 2016-17.

EPS for the current year is trending at 3.60 and all the developments stated above are so exciting, that these can substantially increase the discounting factor. The share should do 80 in a year’s time, I figure.

It is my opinion that this waste-wealth, eco-friendly company has a fantastic future (on a global scale) and that long term investors must track its results and consider adding Yash Papers to their core portfolio.

This stock was originally suggested by @chittoorreddy and @shyaamkp

Very nicely explained. U are doing a great job.

Hi Sir,

I am a regular visitor of your blog. They are very informative.

Here with Yash Papers i have noticed 2 negatives, could you advice on it?

1> 100% promoters stack is pledged.

2> debt of approx 137Cr thats 85 – 90% of the market cap.

Is it adviceable to have this in the portfolio ?

Hi Sir,

I feel someone deleted my query which I had posted some hours ago, but nevermind.

I feel Waste-to-Wealth would help the environment to an extent, but to talk about the numericals about the YASH PAPERS –

1. The company has a debt of approx. 136CR, which is almost 85% of its market cap(153).

2. The promoters have pledged 100% of the stock.

I feel this is some negatives about the company. being in debt the interest paid ratio would high, dividend pay would be less and few others.

Please update and educate me in right direction for my research in YP.

No one deleted any comment, please be assured of that.. all comments need approval and I just got to the computer

The world over, plastic tableware is being banned. France has already done it. Yash is trying to capture a slice of the market. Their debt is 72 cr and the DE is 1.32.. I don’t find it a negative considering the potential

Well, there are many companies that have pledged more than 80% of their stock and it is a worry. So, if you are skeptical, please do not invest.

This seems to be a disruption and huge scope for taking up market share. Going forward these would be secular themes that will be making money. Sir as per MC D/E is too high 2.28. LT D/E is 1.32 which is high for that small base. PE a bit high when compared to Peers.

We have to watch Q2. Company has started reporting record production numbers. Tomorrow is their new brand launch.

sir where is ur analysis for ruchira and alufluoride

Alufluoride I tweeted.. Ruchira, no time for analysis yet – an informed source has recommended

Apologies, my intention was to understand about can these things go against the scrip in near term?

Sir,this stock converting money to paper,May I know reason of falling down ?

This article was written when Yash Papers was 38. Subsequently it went to 80+. So what I wrote proved true. Of course, markets are down now and so is the stock. I’m out of the stock and am unsure of the reasons. Why don’t you read up and post?

nice post .. thanks for sharing …